New Analysis: Residential Protection Initiative Primarily Affects Pension Funds

![[Translate to Englisch:]](/assets/group/_processed_/8/0/csm_AdobeStock_345386520_d9e751892f.jpeg "[Translate to Englisch:]")

In June, the voters of Zurich will vote on the Residential Protection Initiative. It aims to grant municipalities far-reaching intervention rights in the case of renovations, refurbishments or conversions of rental apartments. What is intended as protection for tenants would, according to an initial analysis by Swiss Finance & Property Ltd (SFP), primarily have noticeable consequences for institutional investors – and thus indirectly for many pension fund policyholders.

Swiss Finance & Property Ltd has conducted the first systematic analysis of the potential impact of the residential protection initiative “Protect Affordable Housing, Stop No-Fault Evictions” based on its investment universe of indirect real estate investments totaling more than CHF 238 billion, and has geographically assessed the exposure in the canton of Zurich. The analysis examined in which municipalities institutional residential properties are concentrated and where, if the initiative is approved, additional regulations could be expected due to low vacancy rates and political majorities. The finding: The share of residential properties in the canton of Zurich is substantial – and a significant portion is located in municipalities where new permit requirements and rent restrictions would likely be introduced.

More regulation instead of more supply

The housing market in the canton of Zurich is tight. Demand has been growing faster than supply for years, vacancy rates are low, and rents are rising. In this context, it is not surprising that political pressure is increasing. Between 2023 and 2024, five cantonal popular initiatives on housing were submitted – all with the declared aim of creating or preserving more affordable housing. On 14 June, Zurich voters will vote on three housing initiatives at the same time.

From the perspective of institutional real estate investors, one striking aspect is that the initiatives barely address the core problem – namely the lack of supply. Instead of facilitating, densifying, or accelerating residential construction, they increasingly interfere with property rights, contractual freedom, and investment decisions. What is politically intended as social protection risks producing the exact opposite effect economically.

The residential protection initiative “Protect Affordable Housing, Stop No-Fault Evictions” is the most far-reaching of these proposals, as it seeks to grant municipalities extensive new intervention rights in the management of residential properties. Municipalities would be given the authority to introduce permit requirements for demolitions, conversions, renovations, changes of use, and the conversion of rental apartments into condominiums. Permits could be tied to conditions limiting rent levels. No-fault evictions could be made more difficult or even prevented.

For investors, this primarily means increasing regulatory uncertainty. Renovations would become harder to plan, and rental potential could only be realized with delays or higher costs. In the short term, valuation adjustments are possible; in the medium term, lower returns are likely.

According to the text of the initiative, for housing protection provisions and conditions to apply, the vacancy rate in the respective municipality must also be below 1.5%.

Where new interventions would be most likely

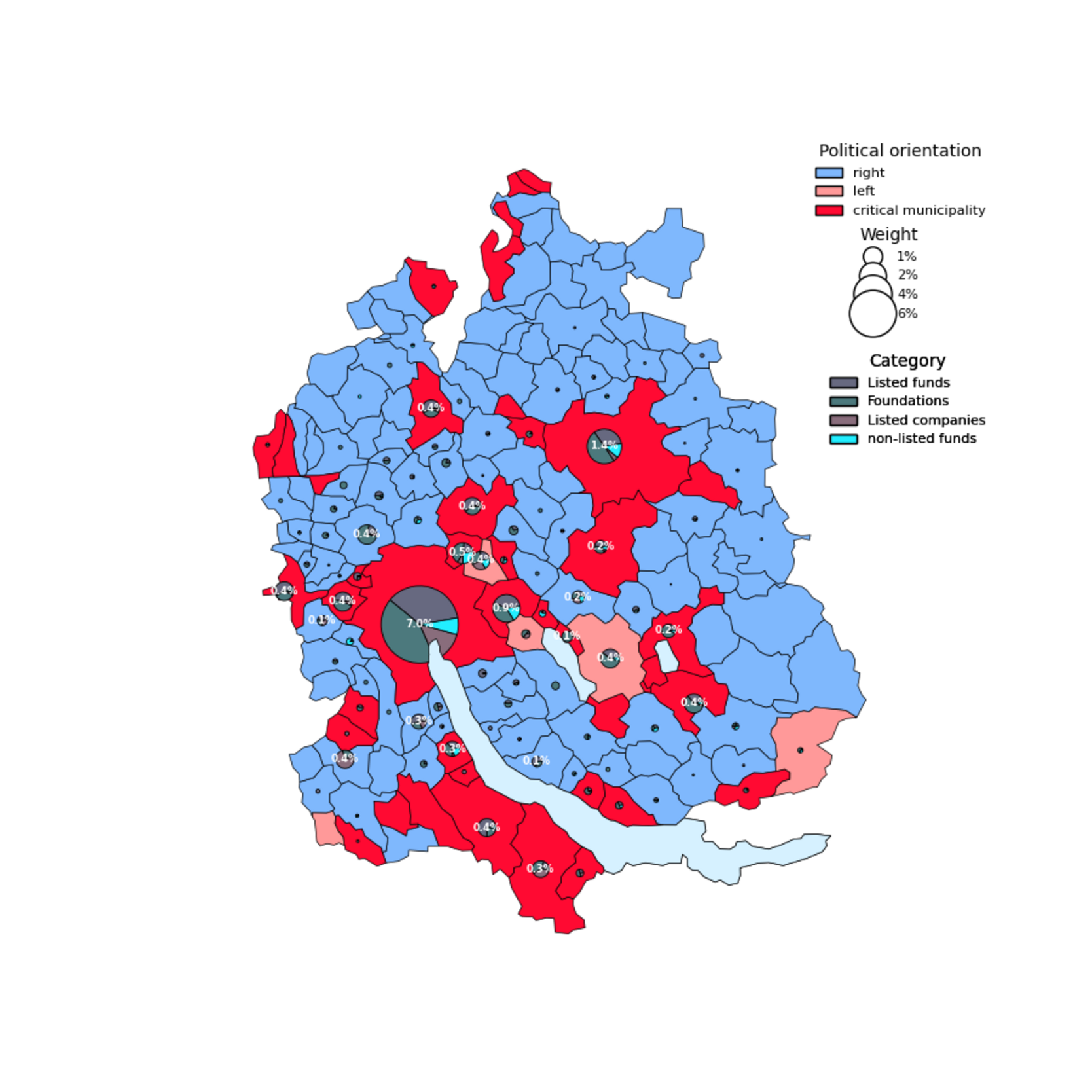

To assess where particularly strict interventions could be expected if the initiative were approved, Swiss Finance & Property Ltd combined two factors. First, it analyzed the political majority situation in municipalities based on the 2023 cantonal council elections. Second, it identified municipalities that have recorded a vacancy rate below 1.5% for three consecutive years – and thus officially qualify as areas with a housing shortage.

Where both criteria coincide – a regulatory-friendly political majority and a structural housing shortage – SFP identifies an elevated risk of additional permit requirements and rent restrictions. Currently, this applies to 46 municipalities. These include the most populous cities in the canton, such as Zurich and Winterthur, as well as numerous other large agglomeration municipalities. Together, they are home to more than half of the population of the canton of Zurich.

Zurich residential properties: Investment foundations are particularly heavily invested

Institutional investors invest not only directly, but also indirectly via real estate funds, real estate companies, and investment foundations in residential properties. The analysis by Swiss Finance & Property Ltd of indirect investments with total real estate assets of CHF 238 billion shows that around 18.1% of these assets are invested in residential properties in the canton of Zurich across more than 100 municipalities.

However, the decisive factor is less the geographical distribution than the question of ownership. The analysis shows that investment foundations – vehicles in which pension funds invest – are particularly strongly engaged in the Zurich housing market. Their share is significantly higher than that of traditional listed real estate companies, which are often at the center of political debate.

Pension institutions, such as pension funds, hold the largest share of these 18% of Zurich residential properties via investment foundations, accounting for more than 8%. They are followed by listed real estate funds with 6.5%, non-listed funds with 1.6%, and listed real estate companies with 2%. Overall, investment foundations have invested 22% of their total real estate assets of CHF 85 billion in residential properties in Zurich.

The real estate companies frequently criticized in the cantonal housing and rental market debate are less heavily invested in the Zurich housing market than often assumed. Only 9.7% of their total real estate assets are allocated to residential properties in Zurich. The share is significantly higher for listed real estate funds at around 18%.

The picture becomes even clearer in the municipalities classified as “critical” – that is, where additional regulations would be most likely if the initiative were approved. In these municipalities, real estate companies hold only 7% of their total real estate assets in residential properties. For investment foundations, the share is 17%, and for listed real estate funds, 15%.

A similar distribution can be observed in the city of Zurich itself: Of the total residential real estate assets invested there, 43% are held by investment foundations and 36% by listed real estate funds. Real estate companies account for only 14%.

The figures thus make one thing clear: Above-average exposure lies primarily with second-pillar investment vehicles, rather than with listed real estate companies.

What approval would mean economically

If the cantonal legislative initiative is approved, it can be expected that institutional investors would face negative consequences in the short term. On the one hand, stricter regulations regarding future rent setting would likely reduce the marketability of properties, leading to value declines. On the other hand, rental potential could be realized more slowly and only at higher cost, which would be reflected in lower returns.

Particularly significant is the fact that a considerable share of the affected properties is held through investment foundations of pension funds and also through funds. Declining valuations and lower income would therefore not primarily affect listed real estate companies, but rather pension institutions – and indirectly the insured members of the second pillar.

Contact

Senior Portfolio Manager Indirect Investments

Senior Portfolio Manager Indirect Investments